Global Logistics Shock: Container Rates Skyrocket

A perfect storm of geopolitical crises, rising fuel costs, and looming regulatory deadlines triggers an explosive surge in global container freight rates.

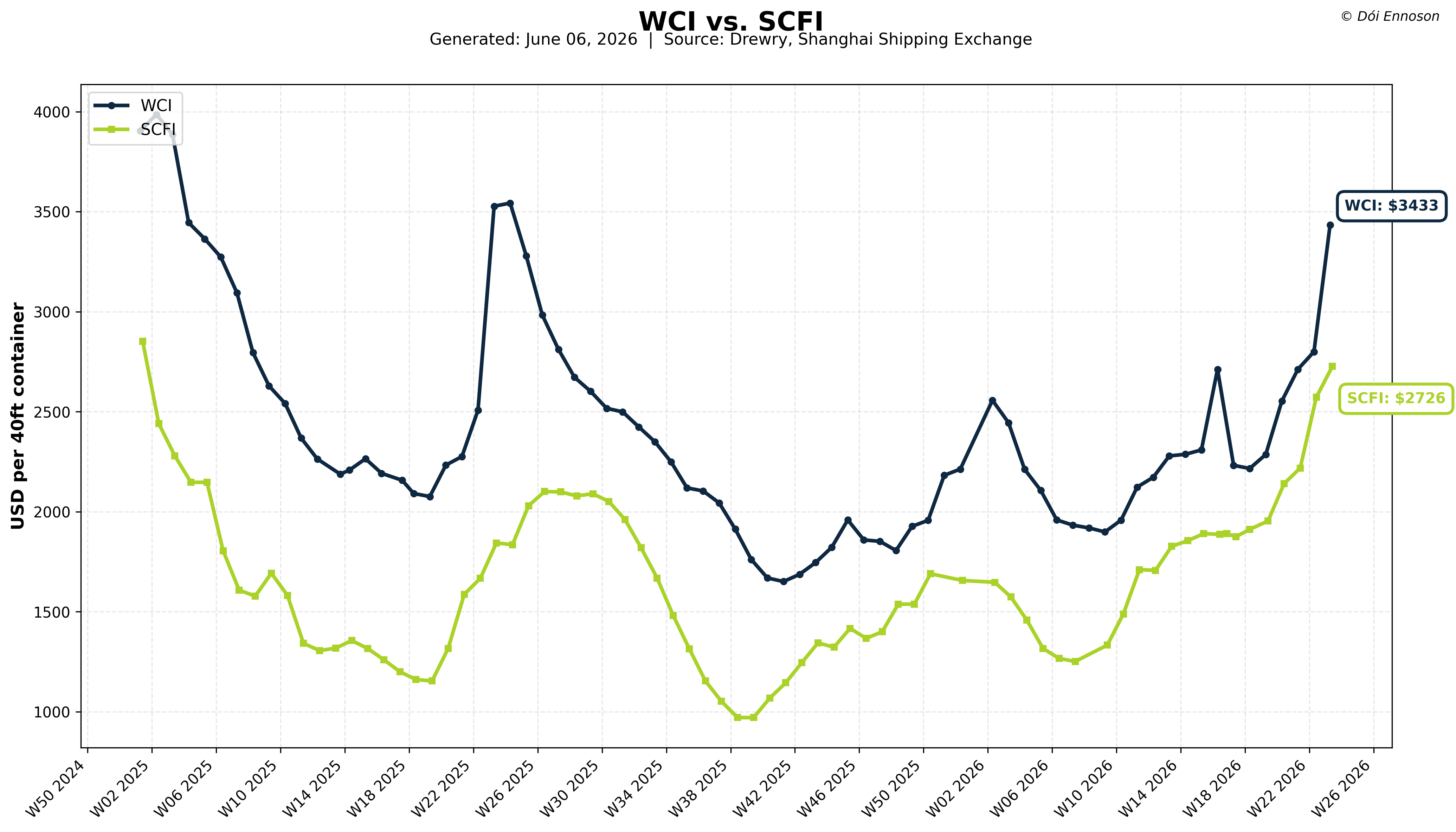

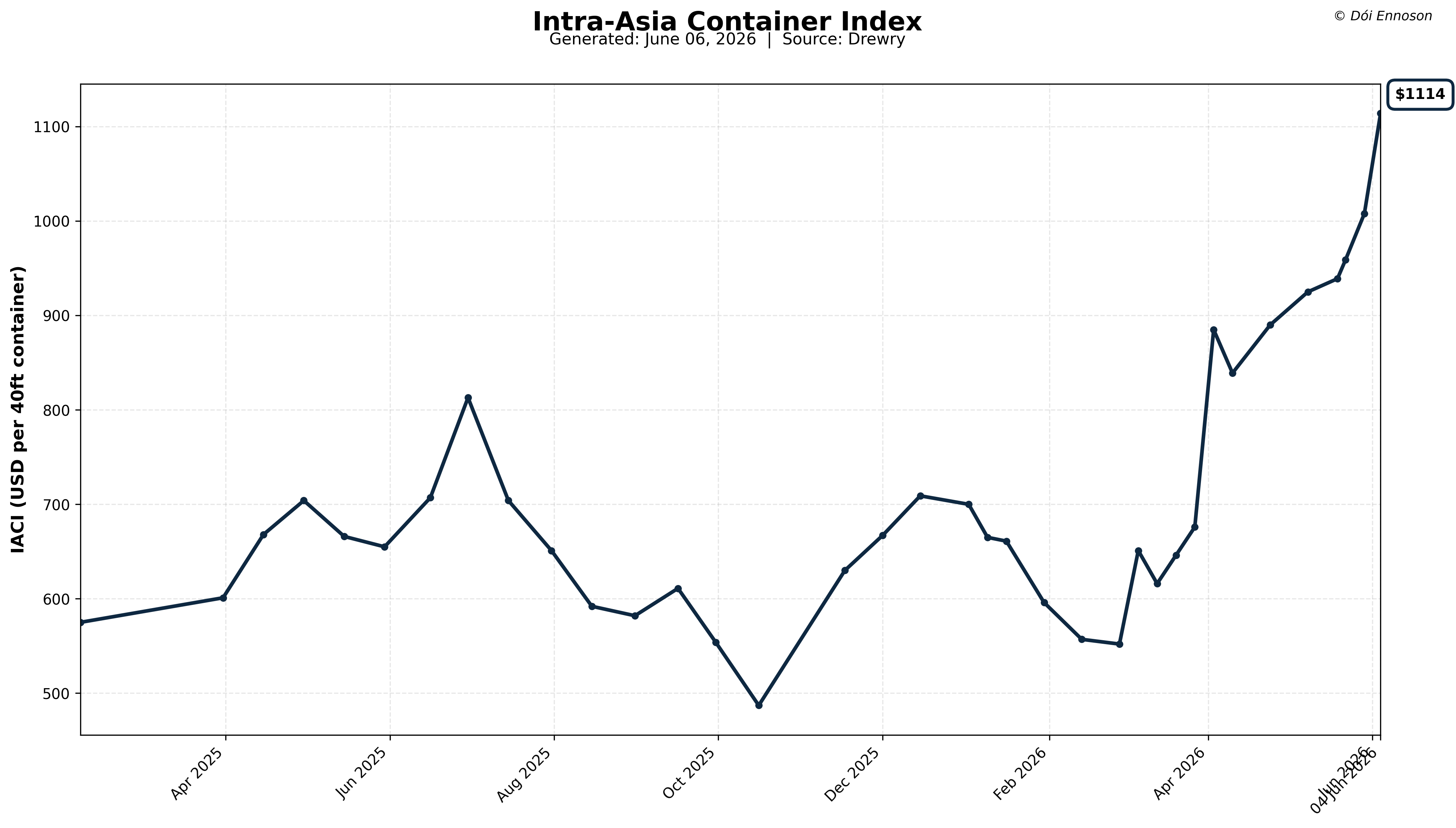

Global supply chains are reeling from yet another severe logistics shock, as the cost of sea freight is rising at record speed to levels that bring back memories of the height of the lockdowns. This latest price surge is starkly reflected in the Drewry World Container Index (WCI), which shot up by 23 per cent in just one week and now stands at $3,433 per FEU. In parallel, the Shanghai Containerised Freight Index (SCFI) climbed by 155 points to a two-year high of 2,726 points, whilst the Drewry Intra-Asia Container Index (IACI) even reached an all-time high of $1,114 per FEU. This is only the fourth time in the history of modern container shipping that freight rates have surpassed the US$1,000 mark within seven days.

The cause lies in the simultaneous convergence of five mutually reinforcing factors. On the supply side, the Hormuz crisis has permanently removed around five to seven per cent of global container freight capacity from the market. On the demand side, the following factors are converging: the bringing forward of shipments ahead of the US customs adjustments in July, the drastic adjustment to the fuel surcharge expected on the same date, the logistics of the FIFA World Cup in North America, the early restocking of retail inventories for summer promotions, and the expiry of the EU de minimis rule on 1 July. On 1 June, these five forces culminated in a coordinated round of price increases by shipping lines. The increased General Rate Increases (GRI) and Peak Season Surcharges (PSS) drove rates up by between US$1,000 and US$1,800 per 40-foot container (FEU) within a single day.

The Hormuz Crisis and Oil Prices Driving Up Freight Rates

The key factor here is that, this time, supply and demand are moving in the same direction at the same time. Whilst the closure of the Strait of Hormuz is reducing available transport capacity, several unrelated factors driving demand are concentrating additional freight into the same period. A market already suffering from capacity shortages is suddenly having to move significantly more cargo. It is precisely this situation that has caused the extreme price spikes of recent weeks.

Since the Strait of Hormuz was closed to commercial container traffic at the end of February, ships have been diverting via the Cape of Good Hope. This adds ten to fourteen days to each voyage. However, this adds up significantly, as each ship completes two to three fewer rotations per year. Extrapolated across the affected fleet, the market is thus short of five to seven per cent of global capacity, amounting to around 1.3 to 1.8 million 20-foot containers.

As the price of Brent crude has jumped from around $80 to as high as $126 per barrel, marine fuel is becoming more expensive for the entire global fleet, not just for vessels that have been rerouted. Shipping companies pass these additional costs directly on to shippers via the Bunker Adjustment Factor (BAF). On the remaining Gulf routes, war risk surcharges of up to US$1,500 per TEU and emergency surcharges of up to US$3,000 per FEU are added. This is precisely where the difference lies compared to the Red Sea crisis of previous years. Back then, the detour alone made transport more expensive; this time, the detour and the oil price are having a combined effect.

New US Tariffs and EU Rules Trigger Surge in Container Traffic

On the demand side, several cost-driving changes are set to take effect on the same date: 1 July. In the US, new tariffs on various imported goods are expected. At the same time, market participants anticipate higher fuel surcharges from shipping companies due to the sharp rise in oil prices. For many importers, this creates a simple incentive: those who ship their goods in June will avoid additional costs.

Shipping before this deadline also avoids both the higher US tariffs and the expected increase in the fuel surcharge. The expiry of the EU de minimis rule means that Shein, Temu, Alibaba and other e-commerce providers are shipping their goods by container to European warehouses before direct shipping of small parcels becomes unprofitable.

The sharp rise in spot rates would be less of a problem for many freight forwarders if long-term transport contracts were still operating as intended. However, in tight markets, this is only the case to a limited extent.

Although annual contracts cushion such fluctuations in quiet periods, when cargo space is in short supply, shipping lines no longer guarantee fixed quotas and give priority to cargo for which GRI and PSS are paid. Shippers with long-term contracts therefore effectively pay the surcharge as well, simply to secure a space at all.

Oversupply of Ships Saves the Market

The behaviour of shipping companies illustrates just how strong demand is at present. Normally, they prop up freight rates through so-called blank sailings, i.e. cancelled sailings. However, during the reporting week, the number of these on trans-Pacific routes fell from eight to three. MSC even reactivated a full service from China to Long Beach. Carriers do not currently need to artificially restrict supply. Demand is strong enough to absorb additional capacity as well.

The impact of the Hormuz crisis now extends far beyond the main shipping routes. Within Asia, too, the flow of goods is changing noticeably. The Drewry Intra-Asia Container Index reached an all-time high during the reporting week. The rate from Shanghai to Mumbai alone rose by 35 per cent. This is due less to the usual peak season than to the diversion of cargo flows that previously passed through the Gulf region. At the same time, the distribution of containers is becoming more uneven. Whilst outbound freight rates are rising, return freight rates from Vietnam and Thailand are falling, as empty containers are being prioritised for return to the major export hubs. This is already creating imbalances that could later lead to a shortage of available containers.

The irony of the current situation is that the supposed oversupply of recent years is now helping to cushion some of the impact. The additional ships, which until recently were seen as a burden on the market, now act as a buffer, preventing an even sharper rise in freight rates.